Transparency and comparability through sustainable disclosure

Guidance on CSRD reporting

Introduction to CSRD

The Corporate Sustainability Reporting Directive (CSRD) is part of the European Green Deal to drive the EU to a green transition and become climate neutral by 2050. The primary objective of the CSRD is enhancing the transparency and comparability of sustainability-related information disclosed by companies.

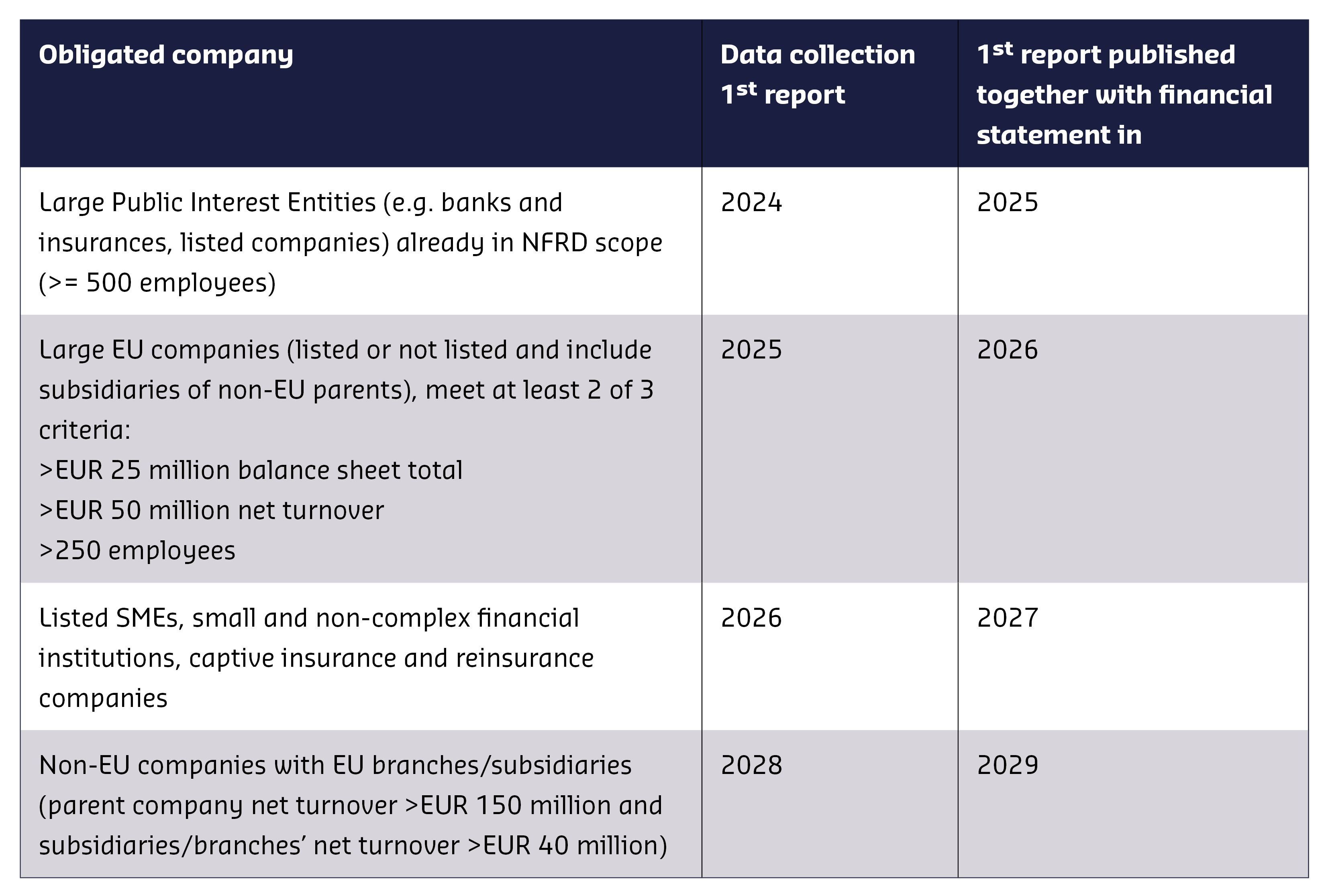

The CSRD becomes applicable for the reporting period starting on January 1st 2024 for companies which were already required to comply with the Non-Financial Reporting Directive (NFRD). The CSRD directive is in fact a successor to the earlier NFRD, with the main difference being increased comparability of reported information between companies, as well as increasing, the number of companies included in the requirement.

Does CSRD apply to me?

CSRD applies to entities falling under the purview of EU law, listed on EU regulated markets, or established within an EU member state. A company is considered large if it meets at least two of the three conditions below:

-

250 or more employees during the financial year

-

€25 million in total assets

-

€50 million in net turnover

Starting from 2025, sustainability reporting becomes mandatory for large companies that were previously outside the scope of the NFRD. Listed SMEs must comply with the CSRD from 2026 onwards, followed by non-listed SMEs.

The CSRD has introduced Financial Materiality, emphasizing the disclosure of material sustainability-related information in financial reports. Initiatives like GRI’s Disclosures on Management Approach (DMA) and ISSB’s Sustainability-related Financial Disclosures (IFRS S1) and Climate-related Disclosures (IFRS S2) further enhance transparency and standardization in corporate reporting, driving accountability and trust among stakeholders.

About the CSRD

The directive requires companies to communicate on the impacts, risks and opportunities of their activities relating to environmental, social or governance (ESG) factors, relying on the principle of “double materiality”.

As per the guidelines of the Corporate Sustainability Reporting Directive (CSRD), conducting a “double materiality assessment” is obligatory for entities mandated to report under the directive. The term ‘double’ is pivotal here, signifying that companies reporting on sustainability must evaluate the significance of a sustainability issue from two distinct viewpoints.

Inside-out and outside-in perspective

On one front, organizations impact both society and the environment (the inside-out perspective), encompassing concerns such as ecological harm and human rights infringements. Conversely, sustainability-related shifts and occurrences unveil (new) risks and opportunities for organizations (the outside-in perspective). Examples include reputation vulnerabilities stemming from corruption incidents, the implementation of fresh CO2 tariffs, or openings for the creation of circular and sustainable products.

Key components

As a full-service sustainability consultancy, Peterson can support companies to publicly disclose:

-

Information about their impacts and challenges in relation to environmental, social and governance matters (impact materiality)

-

How these impacts affect the business itself (financial materiality), based on the principle of “double materiality”

How you benefit

How can Peterson support you?

Our experts in ESG reporting and sustainable finance are highly skilled in assisting companies in their journey to comply with the CSRD regulation. A crucial part of this assessment process is identification of and engagement with stakeholders and users and ensure that a sustainability due diligence process is implemented within the business. We support organizations with the entire reporting process in accordance with the European Sustainability Reporting Standards (ESRS) developed by the European Financial Reporting Advisory Group (EFRAG) to disclose material impacts, risks and opportunities in relation to environmental, social, and governance sustainability matters.

Compliance with the Corporate Sustainability Reporting Directive (CSRD) ensures organizations meet legal requirements while enhancing transparency and accountability to stakeholders. Embracing the CSRD drives sustainable practices, mitigates risks, and fosters innovation, positioning businesses for long-term resilience and competitive advantage in an increasingly ESG-focused environment.

Do you want to know more?

Please contact us so we can help you with your sustainable challenges or certification implementation. Or do you have other questions? We will be glad to help.